Last verified: 30 April 2026

On 1 April 2025, a Mumbai-headquartered tier-1 Indian law firm celebrated its 25th anniversary by elevating eight Counsels to Equity Partner. The firm’s equity bench reached 142. For anyone trying to map the law firm partnership track in India, those numbers are the starting clue, not the headline.

That headline hides the actual story. Each of those eight had spent roughly eight to ten years inside the firm. Some had spent longer. The Counsel tier itself is a four-to-six-year stop-gap, and behind every promotion sits a partnership vote, a sponsoring senior partner, a portable book of business, and the quiet practice-area lottery (four of the eight came from corporate; one each from banking and finance, dispute resolution, projects, and TMT). This isn’t a fairy tale. It’s a sequence of structural decisions, most of which the average associate doesn’t see.

Zoom out and the pattern sharpens. In the same April 2025 cycle, Khaitan & Co promoted 30 lawyers to Partner and 20 to Counsel. Cyril Amarchand Mangaldas elevated 18. JSA, IndusLaw, and Shardul Amarchand Mangaldas all ran formal partnership rounds. Indian firms now run annual promotion cycles at scale, the kind of structural machinery once unique to Magic Circle and US BigLaw houses. And yet the average time to partner has barely moved: the 2014 Legally India study found 9.1 years across CAM, AZB, JSA, Khaitan, Luthra, and Trilegal, and 2025 forum data shows the same 9-to-13-year band for equity partner. Firm sizes doubled, leverage ratios shifted, and the Counsel tier became permanent. The clock didn’t.

So if you’re an associate in 2026 wondering when your turn comes, or whether it will ever come, this is the roadmap. Four big questions sit underneath every detail in this guide. How long does it really take? How much can you actually earn? How does the partnership decision get made behind the closed-door committee meeting? And if it doesn’t happen, what then? Let’s start with the snapshot.

The law firm partnership track in India typically runs 8 to 10 years from law-school graduation to non-equity partner at a Tier-1 firm, and 9 to 13 years to Equity Partner. The path moves through Associate (PQE 0-3), Senior Associate (3-5), Principal Associate (5-7), Counsel or Salaried Partner (7-9), then Equity Partner. Compensation, capital buy-in, voting rules, and sponsorship vary firm by firm.

What that 8-13 year window actually looks like, firm by firm, PQE by PQE, in 2026 rupees, is where every existing guide on the Indian internet stops. The rest of this roadmap fills the gap.

How long does it take to make partner at an Indian law firm?

Most associates can’t get a straight answer to this question, and the reason is simple: the answer depends on the firm, the practice area, and what you mean by “partner.” On the law firm partnership track in India, the honest range is 8 to 10 years to non-equity partner, and 9 to 13 years to Equity Partner, at a Tier-1 Indian firm. At full-service mid-tier firms the band stretches to 10-14 years for equity. At the Big 4 legal arms (EY, Deloitte, PwC, KPMG) it can run 15-16 years.

The 8 to 13 year reality, and why the average has held since 2014

In 2014, Legally India ran the most thorough study of the partnership track ever published in India. The headline number, 9.1 years on average across CAM, AZB, JSA, Khaitan, Luthra, and Trilegal, became the canonical reference. A decade later, that average has barely moved. Forum data from 2025 shows the same 9-to-13-year band for equity partner. Firm sizes doubled. Leverage ratios shifted. The Counsel tier became a permanent fixture. But the clock didn’t.

Why? Three reasons. First, the partnership funnel is structural, not cultural; firm economics dictate how many partners can be carried per associate cohort. Second, the substance of what makes a partner (commercial judgement, originated revenue, team management, client trust) takes roughly a decade to season regardless of training quality. Third, even when associates compress technical learning with AI tools, the relationship-building and book-building parts of the job remain stubbornly human and stubbornly slow.

What “making partner” actually means in 2026

Calling it “one promotion” hides three separate gates. Salaried Partner is a designation upgrade that may carry a partnership business card but no profit share or vote. Non-Equity Partner (NEP) typically draws a fixed compensation plus bonus, with limited or no firm equity. Equity Partner is the real ownership rung: capital contribution, vote, profit share, downside risk. At many Tier-1 firms you cross all three gates over a two-to-four-year stretch, not a single anniversary.

How to read this guide (skim map by PQE)

If you’re at PQE 0-3, focus on the hierarchy section, the 8-step roadmap, and the self-assessment checklist for your band. If you’re at PQE 4-6, read the book-of-business section, the firm-by-firm comparison, and the lateral-calculus section. If you’re at PQE 7-9, the partnership-decisions section, the compensation deep-dive, and the off-ramps section will repay your time. The full 7,000-word read is built for the associate who wants to plan a 10-year law firm partnership track in India in one sitting.

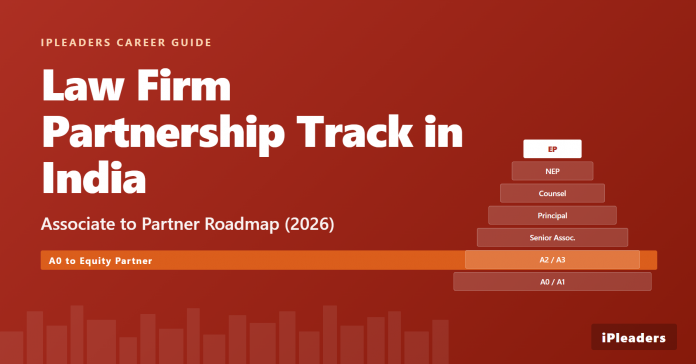

The Indian law firm hierarchy: A0 to Equity Partner, decoded

The same designation can mean three different things at three different firms. So before any track-planning makes sense, you need the canonical map.

The 11 rungs explained

Here’s the standard ladder used at most Tier-1 Indian law firms in 2026.

- A0 (Associate, PQE 0): fresh law-school graduate, just enrolled with a Bar Council.

- A1 (Associate, PQE 1): first promotion, usually based on an annual review.

- A2 (Associate, PQE 2): increased deal ownership, drafting, and supervised client contact.

- A3 (Associate, PQE 3): leading sub-workstreams, mentoring A0/A1, first taste of client meetings.

- Senior Associate (SA, PQE 3-5): full deal-team responsibility, drafting ownership, billing oversight.

- Principal Associate (PA, PQE 5-7): running matters end-to-end, supervising teams of 4-6, beginning intra-firm BD.

- Counsel (PQE 6-8): formal mid-to-senior tier; varies sharply by firm (see firm comparison below).

- Salaried Partner (PQE 7-9): partnership designation, fixed pay, no profit share or vote at most firms.

- Non-Equity Partner (PQE 8-11): structured pay plus bonus, partial governance say at some firms, no capital contribution.

- Equity Partner (PQE 9-13): capital contribution, profit share, vote, full firm ownership rung.

- Senior Equity / Practice Head / Managing Partner (PQE 13+): leadership and governance roles on top of equity.

PQE bands at every rung

Use these PQE bands as planning anchors, not deterministic gates. A high-performer in a hot practice can compress two rungs by a year. An associate parked in a slow team can stretch a rung by two years.

The standard jumps to flag are: A3 to SA (technical-depth gate), SA to PA (deal-ownership gate), PA to Counsel/SP (book-and-BD gate), and NEP to EP (capital-and-sponsorship gate). Each gate has a different rejection reason. Confusing them costs years.

This is also where you’ll find non-lawyer partnerships under the Indian Partnership Act come up, mostly at consulting-style legal services entities rather than traditional law firms. Bar Council and law-firm conduct rules push almost all firm partners to be enrolled advocates, even though the Partnership Act doesn’t require it.

What “Principal Associate” really is

PA is the most misunderstood rung in Indian law. At Trilegal and CAM, it’s a real promotion stop where firms watch for partnership-track signals. At some other firms it’s a parking slot, where high-performing PQE-5-to-7 associates sit for two-to-three-year stretches without a Counsel or Salaried Partner offer in sight. The cleanest tell? Ask the firm what percentage of past PA cohorts converted to Counsel or partner within three years. If the firm dodges, it’s a parking slot.

How firms differ on rung names

Here’s how the top seven firms label their rungs (2025-26 nomenclature).

| Rung (canonical) | CAM | Khaitan & Co | Trilegal | SAM | JSA | AZB | Luthra |

|---|---|---|---|---|---|---|---|

| Senior Associate | Senior Associate | Senior Associate | Senior Associate | Senior Associate | Senior Associate | Senior Associate | Senior Associate |

| Principal Associate | Principal Associate | Principal Associate | Principal Associate | Principal Associate | Principal Associate | Senior Associate (long band) | Principal Associate |

| Counsel | Counsel | Counsel (formal tier) | Counsel | Associate Partner / Counsel | Counsel | Counsel (selective) | Counsel |

| Salaried Partner | Partner (decision) | Partner | Partner | Salaried Partner | Partner | Partner | Partner |

| Non-Equity Partner | (rolled into Partner) | Partner | Partner | (rolled) | Partner | Partner | Partner |

| Equity Partner | Equity Partner | Equity Partner | Equity Partner | Equity Partner | Equity Partner | Equity Partner | Equity Partner |

The takeaway: don’t use rung name as a proxy for power. A Counsel at Khaitan or Trilegal often has more deal autonomy than a Non-Equity Partner at a smaller firm. Always ask what the rung means at that firm.

Top of pyramid – narrow

-

Senior Equity / Practice Head / Managing Partner

PQE13+

INR 4 crore+ -

Equity Partner

PQE9-13

INR 1.5-4 crore -

Non-Equity Partner

PQE8-11

INR 1-1.5 crore -

Salaried Partner

PQE7-9

INR 80 lakh – 1.2 crore -

Counsel

PQE6-8

INR 50 lakh – 1.2 crore -

Principal Associate

PQE5-7

INR 40-70 lakh -

Senior Associate

PQE3-5

INR 28-50 lakh -

A3

PQE3

INR 24-36 lakh -

A2

PQE2

INR 20-30 lakh -

A1

PQE1

INR 16-26 lakh -

A0

PQE0

INR 12-22 lakh

Base of pyramid – wide

The 8-step roadmap from associate to partner in India

If you want a one-page action sequence for the law firm partnership track in India, here it is. Eight steps, each with a PQE marker and a what-to-do core.

- Build technical depth in PQE 1-3. Pick one practice area, run with it. Master the templates, the regulators, the case law cycle. This is the gate to Senior Associate.

- Earn deal ownership in PQE 3-5. Stop being the researcher; become the drafter. Own a workstream end-to-end. Review junior associates’ work. This is the Senior Associate to Principal Associate gate.

- Start visible BD in PQE 4-5. Yes, that early. Write a client alert. Speak at one industry forum. Attend one client breakfast. Get your name on the firm’s regulatory tracker. This is where you separate from the technically-good-but-invisible peer group.

- Build a sponsoring senior partner relationship by PQE 5-6. Identify the partner who will fight for you in committee. If no one is willing to sponsor, that’s a signal to course-correct or switch firms.

- Take ownership of intra-firm cross-sell by PQE 6-7. Refer clients across practice areas. Origination credit at most Indian firms still flows partly to whoever brings the relationship in, even when the work is executed by another team.

- Originate your first standalone client by PQE 7-8. A client who came to the firm because of you, not despite you. The first one is the hardest. By the second and third, you’re tracking toward Counsel or Salaried Partner.

- Complete the Counsel or Salaried Partner gate at PQE 7-9. This is the platform from which the equity case gets built. Use it to formalise team leadership, retention numbers, and a documented book.

- Make the equity case at PQE 9-13. Document originated revenue, team P&L contribution, capital readiness, and a defined practice-build plan. The vote (or partner-committee decision) follows.

What changes from PQE to PQE: the four phase shifts

Phase one (PQE 0-3) is about depth. Nothing else matters as much. Phase two (PQE 3-6) is about ownership. Hours go up, scope widens, drafting gets serious. Phase three (PQE 6-9) is about visibility. BD, intra-firm trust, sponsor identification. Phase four (PQE 9-13) is about origination. Without your own clients, the equity case won’t survive committee.

Where most associates stall

The two stall points are PQE 4-5 and PQE 7-8. The first is the “good Senior Associate but not yet a leader” trap, where technical skill is great but ownership and BD haven’t started. The second is the “great Counsel but not yet a partner” trap, where billings are strong but originated revenue is thin. Both are correctable, but only if you spot them early.

For ambitious associates aiming to compress this timeline meaningfully, more aggressive timeline strategies for ambitious associates cover the lateral-acceleration play and the practice-pivot play. A Magic Circle or US BigLaw roadmap doesn’t fit the Indian firm structure, so don’t copy-paste.

How partnership decisions actually get made

For most associates the partnership decision is a black box. It shouldn’t be. There are four moving parts: the vote, the capital buy-in, the sponsorship dynamic, and the firm-specific decision model. Each part is being reshaped by AI and by the entry of foreign-firm partnerships, both of which change what “merit” means. We’ll come back to that in the future-trends section. For now, here’s the mechanics.

The partnership vote, and what gets you blackballed

A partnership vote is exactly what it sounds like: existing equity partners vote (often by secret ballot) on whether to admit a new partner. Trilegal famously runs a partnership vote model. JSA also operates on a vote. So do many full-service firms with a flat governance structure. Two reasons candidates get blackballed: a senior partner who feels professionally threatened, or a perception that the candidate hasn’t built relationships across the partnership pool. The fix is years of cross-practice goodwill, not last-minute lobbying.

Capital buy-in

Most equity-partnership firms in India require a capital contribution. The range is wide: INR 25 lakh at smaller firms, INR 50 lakh to 1 crore-plus at top-tier firms, depending on the equity unit being acquired. Most firms allow the buy-in to be paid from accumulated bonuses, or financed through firm-arranged loans repaid against profit share over three-to-five years. If you can’t pay, the firm rarely waives. They’ll route you to NEP or Counsel instead.

The sponsorship math

Here’s the uncomfortable truth from forum threads (Legally India 259678 is the canonical one): without a senior partner publicly backing your case in committee, the equity nomination usually doesn’t survive. “No godfather” rarely means “no offer at all,” but it does usually mean “no equity, only Counsel or NEP.” The only counter is a portable book of business so strong that the firm can’t afford to lose you to a competitor. That’s a small, hard-to-reach minority.

Vote vs decision: Trilegal’s process vs CAM’s promotion-by-decision model

Trilegal’s vote-based model means a candidate has to win 60-70% support across the equity bench (specific thresholds vary). CAM, by contrast, runs a managing-partner-and-committee model: the senior leadership decides, the rest of the firm is informed. Neither is universally better for candidates. Vote-driven firms reward broad relationships; decision-driven firms reward strategic alliance with whoever runs the cycle.

| Firm | Vote? | Buy-in | Sponsorship matters? | Typical decision month |

|---|---|---|---|---|

| Trilegal | Yes (partnership vote) | INR 50 lakh – 1 crore band | Critical | March-April |

| CAM | No (MD + committee) | Required | Critical | April |

| JSA | Yes | Required | Critical | March-April |

| Khaitan & Co | Committee + sponsor model | Required | Critical | March |

| SAM | Committee | Required | Important | January-July (multi-cycle) |

| AZB | Founder/committee | Required | Important | Annual cycle |

| Luthra | Founder/committee | Required | Important | Annual cycle |

What goes wrong: assuming merit alone wins. It doesn’t, never has, and probably won’t. Build the technical case, build the book, and build the sponsorship coalition. All three. Pretending one of them is optional is the single most expensive mistake associates make.

Firm-by-firm partnership track: CAM, AZB, Trilegal, Khaitan, JSA, SAM, Luthra (2026)

This is the section associates wish they’d had three years before they made firm choices. Here’s the side-by-side comparison of the law firm partnership track in India across the top seven firms, drawn from 2025 and early 2026 promotion data and Vahura’s compensation tracker.

| Firm | Avg PQE to NEP | Avg PQE to EP | Parallel track | 2025-26 round size | Decision model |

|---|---|---|---|---|---|

| CAM (Cyril Amarchand Mangaldas) | 8-10 | 9-12 | Counsel | 18 partners (April 2025) | Decision by managing partner |

| AZB & Partners | 8-10 | 9-12 | Counsel (selective) | Annual cycle | Decision by founders |

| Trilegal | 7-9 | 8-11 | Counsel-to-EP channel | 8 to EP (April 2025) | Partnership vote |

| Khaitan & Co | 9-11 | 10-13 | Counsel (formal tier) | 30 partners + 20 counsel (March 2025) | Committee with homegrown emphasis |

| JSA | 9-12 | 10-14 | Counsel | 7 to EP (April 2026) | Partnership vote |

| SAM (Shardul Amarchand Mangaldas) | 8-10 | 9-12 | Associate Partner / Counsel | 12 SP + 9 EP + 107 PA/SA (2025) | Decision by managing partner |

| Luthra | 9-11 | 10-13 | Counsel | Annual cycle | Founders / committee |

Cyril Amarchand Mangaldas

CAM’s average to partner sits near the 9.1-year baseline from the 2014 study; the April 2025 round elevated 18 lawyers across Mumbai (9), Delhi-NCR (4), Bengaluru (4), and Hyderabad (1), heavy on corporate (8) with finance (6), dispute resolution (3), and capital markets (1) rounding it out. CAM uses a Counsel rung but doesn’t rely on it as a primary partnership-track waypoint. Origination credit and managing-partner sponsorship are the two big variables.

AZB & Partners

AZB’s culture is lateral-friendly relative to peers. The firm runs an annual cycle and is founder-led on the decision side. Senior associates and counsels regularly move in from CAM, Trilegal, and Luthra and convert to partner within two-to-three years. Track length to NEP is 8-10 years, similar to CAM.

Trilegal: the shortest track in India

Trilegal historically runs the shortest partnership track among Indian Tier-1 firms, averaging 8 years to partner per the 2014 Legally India study and confirmed by 2025 forum data. The April 2025 round moved 8 Counsels to Equity Partner (4 corporate, 1 each in B&F, dispute resolution, projects, TMT). Trilegal’s Counsel-to-EP channel is the cleanest example of a parallel track that actually converts. Total equity bench reached 142 in April 2025.

Khaitan & Co: 30 + 20, homegrown emphasis

Khaitan’s March 2025 round was the largest single annual leadership promotion disclosed in India that year: 30 to Partner and 20 to Counsel. Practices spanned corporate, dispute resolution, tax, banking and finance, capital markets, private equity, and real estate. Senior leadership publicly emphasised that “the majority of leadership is homegrown.” If you want a long, structured, internally-grown track, Khaitan is the canonical bet. Track length is on the longer end (9-11 to NEP, 10-13 to EP).

JSA, SAM, Luthra, IndusLaw, ELP

JSA promoted 7 to Equity Partner in April 2026 (total to 66) and runs on the longer end (10-14 to EP), partly because of partnership-vote thresholds. SAM ran multiple cycles in 2025 (12 salaried partners + 3 counsels in one cycle, 9 equity partners in another, plus 107 PA/SA promotions). Luthra runs an annual cycle, founder-driven. IndusLaw promoted 4 in April 2025. ELP uses Associate Partner as a parallel track and has absorbed lateral hires from AZB and other peers as partners directly.

The pitfall in this section is firm-shopping by track length alone. A short track at Trilegal won’t help if your practice is litigation-heavy; Trilegal weights corporate. A long track at Khaitan is offset by deeper sponsorship and a bigger Counsel runway. Always check track length against practice-area weighting at each firm.

| Firm | PQE to NEP | PQE to EP | Parallel tracks | 2025 promotion round | Decision model |

|---|---|---|---|---|---|

| CAM | 8-10 | 9-12 | Counsel | 18 partners | Decision by managing partner |

| AZB | 8-10 | 9-12 | Counsel | Annual cycle | Decision by founders |

| Trilegal | 7-9 | 8-11 | Counsel-to-EP | 8 to EP | Partnership vote |

| Khaitan & Co | 9-11 | 10-13 | Counsel formal | 30 partners + 20 counsel | Committee + homegrown emphasis |

| JSA | 9-12 | 10-14 | Counsel | 7 to EP (April 2026) | Partnership vote |

| SAM (Shardul Amarchand) | 8-10 | 9-12 | Associate Partner / Counsel | 12 SP + 9 EP + 107 PA/SA | Decision by managing partner |

| Luthra | 9-11 | 10-13 | Counsel | Annual cycle | Founders / committee |

Parallel tracks: Counsel, Of Counsel, Director, Principal Counsel, Associate Partner, Responsible Partner

Associates who haven’t navigated this terrain often ask, “Am I on a real path or a parking lot?” The honest answer depends on which firm you’re at and which parallel track you’re being offered.

Counsel and Of-Counsel: who uses them, what they actually do

Counsel is now a formal mid-to-senior tier at Khaitan (formal Counsel rung), Trilegal (Counsel-to-EP channel), ELP (Associate Partner equivalent), IndusLaw (Counsel role), and SAM (Associate Partner / Counsel). At Trilegal it’s a real partnership-track waypoint: the April 2025 round elevated 8 Counsels to Equity Partner directly. At Khaitan it’s a formal rung with structured progression. At some other firms it functions more like a long-tenure perch for technical experts who don’t want partnership economics.

Of-Counsel is different. It’s typically a senior practitioner attached to the firm without partnership economics, voting rights, or capital contribution. Often used for retired partners staying engaged, or for senior in-house lawyers brought in part-time. Don’t confuse Counsel and Of-Counsel: the economics, hours, and trajectory are different.

Associate Partner / Director / Principal Counsel: the new tiers

Several firms have introduced Associate Partner (SAM, ELP), Director (Big 4 legal arms), and Principal Counsel (a few mid-tier firms) as additional rungs. The intent is to retain high-PQE talent that hasn’t built a book yet, by offering a partnership-adjacent designation without equity. Some of these tiers convert to partner; others are deliberately permanent perches. Ask, before accepting, what percentage of past holders converted within three years.

Responsible Partner (“RP”): Legally India’s open secret

The RP role surfaces in Legally India forum thread 206094 and in 14-15-year holdout discussions. An RP is a senior lawyer responsible for client portfolios and team P&L without being granted full equity. Not all firms use the term, but several mid-tier firms operate functional equivalents. If you’re offered an RP-style role, ask for the time-bound conversion plan to equity.

Counsel vs Salaried Partner: which is more secure?

Counterintuitive answer: at some firms Counsel is more secure than Salaried Partner. Counsel is typically a recognised senior expert role with stable pay (INR 50 lakh to 1.2 crore at top firms, per Vahura tracker). Salaried Partner is a designation rung where pay can be similar (INR 80 lakh to 1.2 crore) but expectation is that you build a book quickly or get rotated. The pitfall: accepting a Counsel offer because the title sounds prestigious, then realising the firm has no path from there to partnership.

Here’s the parallel-track usage map across the top firms.

| Firm | Formal Counsel? | Of-Counsel? | AP / Director? | RP? | Typical conversion to partner |

|---|---|---|---|---|---|

| Trilegal | Yes (Counsel-to-EP) | Limited | No | No | High (April 2025 saw 8 Counsels to EP) |

| Khaitan & Co | Yes (formal tier) | Yes | No | Limited | Moderate-high (homegrown emphasis) |

| CAM | Yes | Yes | No | No | Moderate |

| SAM | Yes | Yes | Yes (AP) | No | Moderate |

| ELP | (AP used) | Yes | Yes (AP) | No | Moderate |

| IndusLaw | Yes | Yes | No | No | Moderate |

| AZB | Selective | Yes | No | No | Moderate |

Partner compensation decoded: salaried, non-equity, equity, and “eat what you kill”

Compensation is where most Indian-internet content goes vague. Vahura’s 2024-25 compensation report, combined with firm press release patterns and Legally India forum threads (364847 and 399431), lets us anchor real numbers.

Salaried partner vs equity partner: the 50-word definition pair

A salaried partner draws fixed pay plus bonus, doesn’t share in firm profits, and typically doesn’t vote on partnership matters. An equity partner contributes capital, shares in firm profits, votes on key decisions, and bears downside risk. Salaried partner is a waypoint at some firms and a permanent designation at others. Equity is the real ownership rung.

2024-25 compensation bands at every PQE

Per Vahura’s India Law Firm Compensation Trends 2024-25, here’s the PQE-to-pay map.

| PQE band | Large-firm median (INR) | Mid-sized firm median (INR) | Boutique median (INR) |

|---|---|---|---|

| 0-3 (A0-A3) | 12-36 lakh | 8-22 lakh | 5-18 lakh |

| 3-5 (Senior Associate) | 28-50 lakh | 22-38 lakh | 18-32 lakh |

| 5-7 (Principal Associate) | 40-70 lakh | 32-55 lakh | 25-45 lakh |

| 6-8 (Counsel) | 50 lakh – 1.2 crore | 40-80 lakh | 30-60 lakh |

| 7-9 (Salaried Partner) | 80 lakh – 1.2 crore | 65-95 lakh | 45-75 lakh |

| 10+ (Non-Equity Partner) | 1-1.5 crore | 80 lakh – 1.2 crore | 60 lakh – 1 crore |

| Equity Partner (fresh) | 1.5-4 crore | 1-2 crore | 70 lakh – 1.5 crore |

| Senior EP / Practice Head | 4-10 crore+ | 2-4 crore | 1-2 crore |

Vahura’s headline data point: large-firm 10+ PQE median compensation hit INR 104.9 lakh in 2024-25; mid-sized firms 80.4 lakh; boutique 62.31 lakh. Year-on-year compensation rose 12-20% across firm categories, well above inflation.

Fresh equity partner pay at top firms

Trilegal’s 8 Counsels who became Equity Partners on 1 April 2025 likely landed in the INR 1.5 to 4 crore band as fresh EPs, with the corporate practitioners closer to the upper end given practice-area economics. Senior EPs at top firms clear INR 4 crore comfortably; practice heads and managing partners run INR 6-10 crore-plus, with origination-heavy partners exceeding that.

How partner pay is structured

Indian firm partner pay typically combines: (1) a fixed base, (2) an annual bonus tied to firm-wide profitability, (3) a share of billed hours from the partner’s book, (4) origination credit from clients the partner brought in, and (5) capital return or distribution on the equity unit held. Some firms layer in retention multipliers; a few have started experimenting with “eat what you kill” features at the senior-EP level, where origination credit dominates over partnership-pool sharing. Pure “eat what you kill” remains rare at full-service Tier-1 Indian firms.

Why some non-equity partners earn less than counsels

This is one of the most counterintuitive findings in Indian partnership economics. At certain firms, a senior Counsel with a stable book (INR 1 crore-plus billings) can earn more than a fresh NEP whose pay is tied to a fixed-plus-bonus structure capped below the Counsel’s billing share. The lesson: don’t take the NEP designation just for the title. Compare the actual cash-out structure.

For a deeper breakdown of how some senior associates and counsels earn at or above partner levels, see alternative high-earning paths beyond Tier-1 partnership.

PEP (Profit per Equity Partner): does any Indian firm publish it?

PEP is the benchmark global firms (Magic Circle, US AmLaw 100) publish annually. No Indian firm publicly publishes PEP. Bar and Bench has tracked partial estimates from firm-disclosure documents and Vahura analyses; the back-of-envelope ballpark for top Tier-1 PEP is INR 3-7 crore per equity partner per year, with senior practice heads running materially above. Until firms publish, treat these as estimates, not firm financials.

Equity vs Non-Equity vs Salaried Partner: side-by-side

| Dimension | Salaried Partner | Non-Equity Partner | Equity Partner |

|---|---|---|---|

| Capital buy-in | None | Sometimes (smaller) | Yes (INR 25 lakh – 1 crore+) |

| Voting rights | None | Limited (firm-specific) | Full |

| Profit share | None (fixed + bonus) | Limited (sometimes a small share) | Yes |

| Downside risk | Low | Moderate | High (capital at risk) |

| Typical pay band (Tier-1) | INR 80 lakh – 1.2 crore | INR 1 – 1.5 crore | INR 1.5 – 4 crore (fresh) |

| Exit | Termination = loss of designation only | Termination + capital is rare | Capital return + departure mechanics |

Building a book of business: when, how, and how much

“Build a book” is the most common career advice in Indian law and the least explained. Let’s fix that.

What “book of business” actually means at an Indian firm

A book of business is the client revenue you originated and continue to retain for the firm. At Indian firms it’s typically tracked through two metrics: origination credit (the credit you get for bringing the client in, often shared with the partner who closes them) and retained-client billings (annual billings from clients still actively engaged). Some firms also track cross-sell credit when you refer a client to another practice within the firm.

When to start: PQE 4-5, not PQE 7

This is where conventional advice fails. The standard line is “build a book once you make Senior Associate.” That’s already too late. By PQE 4-5 you should be writing client alerts under your byline, attending one industry forum, and building a relationship with at least one in-house counsel at a target client. The associates who start at PQE 7 are competing against peers who started at PQE 4, and they lose.

How much business is needed for equity

For a fresh Equity Partner at a Tier-1 Indian firm, the typical origination expectation is INR 2-5 crore in annual billings traceable to the partner’s relationships within the first two years of equity. Some firms set a higher bar (INR 5-8 crore) for senior practice areas. The number scales with practice area and city: corporate Mumbai partners need bigger books than dispute resolution Delhi partners.

| BD activity | Start by PQE |

|---|---|

| Read the firm’s client alerts and regulatory tracker | 1 |

| Attend one in-house counsel meet-up per quarter | 2-3 |

| Co-author a client alert with a senior associate | 3-4 |

| Speak at one industry forum | 4-5 |

| Build a documented contact list of 50 in-house counsels | 5-6 |

| Originate the first standalone client meeting | 6-7 |

| Bring in the first standalone retainer | 7-8 |

| Build cross-practice referral pipeline | 8-9 |

What “rainmaker” means in the Indian context

A rainmaker, in the Indian Tier-1 firm sense, is a partner whose originated revenue meaningfully shifts the firm’s annual P&L. The threshold isn’t formally defined, but at most Tier-1 firms a rainmaker brings in INR 15-30 crore per year. Rainmakers are rare; most equity partners maintain books of INR 4-10 crore. The pitfall: assuming you need to be a rainmaker to make equity. You don’t. You need to be a credible originator with sustained retention.

The numbers behind the track: pyramid economics, gender ratio, leverage

The partnership funnel feels open from PQE 0. It isn’t. It’s structurally closed by leverage math.

The pyramid truth: leverage ratio, why most associates can’t make partner

Indian law firm leverage ratios have shifted over the last decade. In 2016 most Tier-1 firms ran 1:4 partner-to-fee-earner ratios. By 2025, that’s closer to 1:6 to 1:8 at the largest firms. Khaitan’s 1,200+ legal professionals against ~300+ “leaders” is a useful proxy. Mathematically, at a 1:6 ratio, only roughly 16% of any associate cohort can ever become partner just by structural availability of slots, before merit even enters the conversation.

| Firm (proxy) | Approx fee-earners | Approx partners/leaders | Leverage ratio |

|---|---|---|---|

| Khaitan & Co | 1,200+ | 300+ | ~1:4 (broad leadership), tighter for EP |

| CAM | 800+ | 150+ | ~1:5 |

| Trilegal | 600+ | 142+ EP (April 2025) | ~1:4 EP, tighter overall |

| SAM | 750+ | ~180+ partners across SP/NEP/EP | ~1:4 |

| Leverage ratio | What it means for cohort odds |

|---|---|

| 1:4 | ~25% of associates can reach partner over a career |

| 1:6 | ~16% structural ceiling |

| 1:8 | ~12% structural ceiling |

The lesson: the math is the math. You can be excellent and still not make partner because the slot wasn’t available the year you were ready. This is also why what early-career associates rarely hear about big-law internships matters: the funnel narrows hard from PQE 5 onwards.

Gender ratio at top 30 Indian law firms

Approximately 30% of partners across India’s top 30 firms are women, per Legally India and Bar and Bench data. The ratio drops to roughly 15% in litigation seniority. Outliers exist; Samvad Partners has reported approximately 64% women partnership. The ratio improves at junior associate levels (close to parity at A0-A3) and compresses sharply at Counsel-and-above. The structural reasons (partnership timing colliding with childcare years, fewer women senior partners as sponsors) are well-documented.

Big 4 (EY/Deloitte/PwC/KPMG) partnership track vs Indian law firms

Big 4 legal arms run 15-16 year partnership tracks, materially longer than the Indian Tier-1 firm 9-13 year band. The reason is structural: Big 4 partner cohorts are smaller relative to the consulting parent’s scale, and capital contribution at Big 4 partner is significantly higher (often INR 1-3 crore-plus). For a corporate associate weighing options, the Indian Tier-1 firm is the faster track. For a tax or transfer-pricing specialist, Big 4 may offer better practice depth.

PEP and firm economics: the data Indian firms don’t publish

As noted in the compensation section, no Indian firm publicly publishes PEP. The estimated INR 3-7 crore-per-equity-partner band at top Tier-1 firms is back-of-envelope math from billing patterns and partner promotion press releases. Watch for one of the larger Indian firms to publish formal PEP data within the next 2-3 years; capital-market-listed peers globally are pressuring firms toward disclosure.

A non-NLU graduate can absolutely make partner; the 2014 Legally India study and 2025 promotion data show NLU dominance is real but not absolute. What matters is the firm you join at A0 and the practice depth you build in PQE 0-5.

BCI rules and the foreign firm effect: 2023 rules + May 2025 IFLF clarification

This is the section every other guide skipped. The Bar Council of India‘s foreign-firm rules, published on its official website, are the single most important regulatory shift on the partnership track in a generation.

The March 2023 BCI rules

In March 2023, the BCI notified rules permitting foreign lawyers and foreign law firms to register and operate in India on a reciprocity basis. The scope is narrow: foreign and international law only, not Indian law, and not appearance in Indian courts. This was the first formal liberalisation of the Indian legal market in its modern history. Several international firms began evaluating registrations in 2023-24.

The May 2025 IFLF (Indian-Foreign Law Firm) clarification

In May 2025, the BCI brought into force amended rules introducing the IFLF (Indian-Foreign Law Firm) concept. The amendment expanded the scope for structured Indian-foreign law firm collaborations and allowed Indian advocates to register as foreign lawyers or foreign law firms while continuing Indian-law practice. For the partnership track, this opens (for the first time) a possible foreign-firm partnership channel for Indian-qualified lawyers. Lexology, Majmudar & Partners, India-Briefing, and SCC Times all flagged this as a meaningful liberalisation step.

A new partnership tier: foreign-firm India office partner economics

Within 2-3 years, several global firms (per Covington, BDO, Vahura analysis) are expected to register under BCI rules. A new “foreign firm India office partner” track will likely emerge, paying in USD or EUR-denominated bands materially above current Indian Tier-1 EP comp. The likely effect is a wage war for senior associates and partners, with Indian Tier-1 firms forced to either match comp or differentiate on culture and equity ownership.

| Period | Regulatory state | Implication for partnership track |

|---|---|---|

| Pre-March 2023 | Closed market | Indian Tier-1 firms uncontested |

| March 2023 – May 2025 | BCI rules notified, limited registrations | Indian firms preparing for entrants |

| May 2025 onwards | IFLF clarification expands collaboration scope | New foreign-firm India office partner tier emerging |

| 2026-2028 (expected) | Multiple international firm registrations | Wage and partnership-track competition intensifies |

The pitfall: assuming foreign-firm partnerships are open to all. They’re not. Litigators are explicitly excluded under current rules. Foreign-firm India offices will primarily hire from corporate, banking and finance, and dispute-resolution-arbitration practices, not court-appearance litigators.

Practice area premiums: corporate vs litigation vs niche specialisation

Practice area choice quietly locks in track length. Most associates don’t realise this until PQE 5, when the data becomes visible.

Corporate practice: fastest track in India, highest 2025-26 promotion volumes

Corporate has consistently been the fastest partnership track in India. Of Trilegal’s 8 April 2025 EP elevations, 4 were corporate. CAM’s April 2025 round of 18 had 8 corporate partners (44% of the cohort). Khaitan’s March 2025 round of 30 was heavily corporate-weighted. The reason is volume: corporate generates the highest billable hours per partner and the most originated client relationships, both of which feed the partnership case directly.

Disputes and litigation: slower, leaner partnership pyramid, different lifestyle

Litigation has a leaner partnership pyramid. Fewer slots, longer tracks (often 11-14 to EP versus 9-12 in corporate), but lower leverage at the partner level (a litigation partner runs smaller teams). Per-partner economics at the senior end can match or exceed corporate, but volume is lower and the partner runway is longer.

Niche specialisation premium

Niche practices (DPDP Act compliance, data protection, ESG, white-collar, fintech, climate law, AI/IP, sports law) command faster partnership tracks because the qualified-candidate pool is shallow. SAM’s July 2025 round of 9 equity partners spanned funds, tax, competition, white-collar, M&A, IP, education, and private client; narrow specialists got equity, generalists less so. Forecast: niche specialists will see a one-to-two-year compression on the track over 2026-2031 as practice areas keep splintering.

| Practice area | Avg PQE to EP | 2025-26 promotion share | Lifestyle comparison |

|---|---|---|---|

| Corporate (M&A / PE / capital markets) | 9-12 | ~45-50% of Tier-1 promotions | High hours; high BD pressure |

| Banking & Finance | 9-12 | ~15-20% | High hours; specialist pull |

| Disputes / Litigation | 11-14 | ~10-15% | Court time; lower leverage |

| Tax | 10-13 | ~5-8% | Specialist; cyclical hours |

| Niche (DPDP / ESG / fintech / IP / climate) | 8-12 (compressing) | ~10-15% | Variable; specialist pull |

The pitfall: chasing a niche too early, before building broad commercial awareness. A DPDP specialist with three years of pure DPDP work and no broader corporate exposure will struggle to make partner because the firm can’t cross-staff them on bigger deals.

The true cost: hours, stress, family, lifestyle

Glamorising partnership ignores the cost. Let’s not do that.

Billable hour reality at Tier-1: 2,200-3,000 logged hours/year

Per LawBhoomi data and Legally India forum patterns, Tier-1 Indian associates log 2,200-3,000 billable hours per year. Total worked hours often exceed 3,500 (research, internal training, BD, admin). That maps to 60-70 hour weeks for most of the year, with peaks above 80 in transaction crunch. Litigation associates’ chargeable patterns differ; court time and case-research time fold in differently.

Lifestyle compression PQE 1-7 and the hidden costs

The PQE 1-7 stretch is where most partner-track associates compress their personal life: delayed marriage, postponed parenthood, fewer hobbies, narrower friend circles. The hidden cost isn’t just time; it’s the compounding effect of seven years of socialisation only with colleagues, which makes lateral career pivots harder later. A generational split is opening up: younger associates raised on AI tools resist 70-hour weeks, while older partners built their books on those hours. Firms that fail to bridge this will lose Gen-Z lawyers to in-house, boutique founder routes, and creator/legal-tech startups.

Once you’re partner, does the stress reduce? (Spoiler: it transforms)

It transforms, doesn’t reduce. Drafting hours drop (junior partners delegate downward). BD pressure rises sharply (you’re now responsible for originating revenue). Team management replaces individual execution as the dominant time sink. Capital risk enters the picture for equity partners. Most fresh equity partners report harder first-year stress than they expected, not easier. The 2,200-hour week becomes a 2,000-hour week, but with different cognitive load.

Burnout signals to watch: persistent disturbed sleep across more than three weeks; loss of interest in work types you used to enjoy; deteriorating client communication quality you yourself notice; relationships outside work fading; physical symptoms (headaches, weight changes) that don’t resolve with weekend rest. If three or more apply for over a month, that’s a signal to course-correct, not a flag to push through.

Future of the partnership track (2026-2031)

The associate who plans a 10-year track without modelling the next five years of change is planning for a market that won’t exist. Here’s what’s reshaping the law firm partnership track in India over the next five years.

AI compresses the associate funnel

Per BDO India and Trilegal partner commentary in 2025, AI tools (VIDUR AI being one of the prominent Indian-built ones) reclaim approximately 30% of billable hours and materially compress research and first-draft cycles. Microsoft’s January 2026 piece highlighted Indian firms moving to AI-assisted research at scale. Junior associate hiring pipelines are slowing per 2025 industry coverage. The implication: leverage ratios will tighten, associate cohorts will shrink, and partnership odds may improve in absolute terms. But criteria will harden around BD and client management, which AI cannot do.

Billable hours hybridise

Trilegal partners and BDO commentary in 2025-26 confirm a move toward value-based and outcome-based billing. Firms that retain pure billable-hour partnership tests will look outdated by 2028-2030. Firms that build “client value created” metrics alongside hours will win the next-generation lawyer. The partnership case in 2030 may include a “value created” line item next to “billable hours” on every promotion file.

Foreign-firm India offices create a new track

As the BCI section explained, expect 2-3 international firms to begin registered operations within 2-3 years. The new “foreign firm India office partner” track will pay in USD/EUR, pulling Indian Tier-1 senior associates and counsels. Indian firms will respond with retention bonuses and equity acceleration for high-performers; some have already begun.

Specialisation premium widens

Niche practices command shorter tracks; this trend will accelerate. By 2031, expect DPDP, ESG, AI/IP, climate, and fintech to each have dedicated practice heads at most Tier-1 firms, with associates who chose those niches early seeing meaningfully shorter tracks (8-10 to EP versus the generalist 10-13).

New rungs may emerge

“Counsel-for-life” tracks (a permanent Counsel role with 40% lower revenue targets and no partnership obligation) are already discussed in Legally India forums. Expect formal versions by 2027-28. Director, Principal Counsel, and Associate Partner tiers may proliferate as firms try to retain high-PQE talent that hasn’t built a book yet.

The new partner profile

The next decade’s partner cohort on the law firm partnership track in India will be the smaller subset of associates who can mentally hold two skills at once: AI-native efficiency and relationship-first business development. That hybrid will be rare and command premium pay. Associates who specialised in being the best researcher will see their currency devalued; the new partner profile is hybrid technologist plus relationship-manager, not analytical specialist.

Stay or switch: the lateral calculus

Most associates flip-flop on the stay-or-switch question with bad data. Here’s the framework.

When moving firms accelerates partnership, and when it kills it

Moving accelerates partnership when (a) you’ve hit a ceiling at your current firm because of leverage or sponsor scarcity, (b) your target firm has a shorter track or a clearer Counsel-to-EP pipeline, or (c) you can move with a portable book or specialist niche. Moving kills partnership when (a) you switch before PQE 3 (treadmill reset), (b) you switch into a firm where you don’t know the senior partners (no sponsor at the new firm), or (c) you switch laterally without negotiating a clear track-length commitment.

Lateral hire vs homegrown: the bias by firm

Khaitan’s “majority is homegrown” emphasis is real. AZB and ELP run more lateral-friendly cultures, with several lateral counsels and senior associates converting to partner within two-to-three years (the AZB-to-ELP corporate-commercial 2025 move is one example). CAM sits in between. JSA and Trilegal lean homegrown but accept high-quality laterals.

The 3-5-7 rule for switching

A useful rule of thumb. Don’t switch before PQE 3 (you reset technical credibility). The optimal first-move window is PQE 5 (you’ve built ownership, you can negotiate, and the new firm sees track potential). PQE 7 is the lateral-as-partner threshold: by then you should be moving as a Counsel-to-Partner candidate, not as a pure associate. Switching after PQE 8 without a partner-level offer signals firm-instability rather than ambition.

The pitfall: switching too early resets the clock; switching too late labels you as “stuck.” Make the move in the PQE 5-7 window if you make it at all.

Off-ramps and alternative paths: what if you don’t make partner (or don’t want to)?

The vast majority of associates won’t make equity partner. That’s not a failure of the law firm partnership track in India; it’s structural pyramid math. The question is what you do instead.

In-house General Counsel: when it’s the better economic deal

General counsels at US-listed MNCs in India earn INR 1.5-3 crore in cash plus RSU at late-30s, with 900-1,100 hour years. Tier-1 firm associates at the same PQE earn comparable cash but log 2,200-3,000 billable hours. The economic logic of staying till partner is breaking, especially because salaried partner pay (INR 80 lakh – 1.2 crore for fresh, 1.5-2.5 crore for experienced) overlaps directly with senior in-house GC pay. Result: firms are accelerating EP pay just to retain candidates, widening the equity vs salaried gap. For a clean breakdown, the in-house counsel vs law firm partner economics breakdown goes deep.

The boutique founder route: break-even economics and 5-year P&L

Starting a boutique law firm typically requires a 12-18 month runway (INR 30-60 lakh personal capital) and 24-30 months to break-even on a small-team setup. Year-one revenue at a credible boutique founded by a PQE 8-12 lawyer with a portable book is INR 1-3 crore; year-three revenue for the same boutique is INR 4-8 crore. The economics work if you bring 3-5 anchor clients and a niche the bigger firms underserve.

Going on your own: independent counsel, chamber practice, litigation independent

Independent counsel and chamber practice are the traditional disputes off-ramp. Independent litigation practitioners with 10-year senior associate experience can build INR 1.5-3 crore practices within 3-5 years if they specialise (commercial arbitration, white-collar, intellectual property litigation). The downside: no firm overhead means no partner support and slower scaling.

Judiciary, academia, legal-tech: the unconventional off-ramps

Judiciary requires Bar Council enrolment and 10-year practice experience for District Judge entry under direct recruitment in most states. Academia (NLU faculty, top private-university law schools) requires LLM/PhD pathway and lower comp (INR 15-40 lakh range). Legal-tech founder roles have grown in 2024-25 with several Tier-1 firm associates building dispute-resolution platforms, contract analytics tools, and regulatory-tracker products.

The Principal-Associate-but-out exit playbook

If you’re a PA who has decided you don’t want partner-track, the cleanest exit is a 12-month plan: (1) document your billing and origination contributions, (2) line up an in-house or boutique role, (3) negotiate a mutual departure that protects your reference, and (4) close transitions cleanly. The worst exit is to drift; firms eventually run quiet performance reviews on PAs who stop showing partnership-track signals, and a managed-out exit is materially worse for your next role than a planned exit.

| Path | Time horizon to peak comp | Peak comp band | Hours/year | Risk profile | Exit options |

|---|---|---|---|---|---|

| Tier-1 EP | 12-15 years | INR 4-10 crore+ | 2,500+ | High (capital + career) | Lateral / in-house / boutique |

| In-house GC at MNC | 10-12 years | INR 1.5-3 crore + RSU | 900-1,100 | Low-moderate | Board roles, advisory |

| Boutique founder | 8-12 years | INR 4-10 crore (variable) | 2,000-2,500 | High (entrepreneurial) | Sale, merger, growth |

| Independent counsel / chamber | 12-18 years | INR 2-5 crore | 1,800-2,400 | Moderate (book-dependent) | Senior counsel designation |

The “Am I on track to make partner?” self-assessment checklist

Aspirational associates desperately want a diagnostic for the law firm partnership track in India. No competitor offers one. Here’s the iPleaders 30-item version, calibrated against Vahura, Bar and Bench, and Legally India forum patterns.

How to use it: tick each item that’s true for you within your current PQE band. 8+ ticks = on track. 5-7 = course-correct. Below 5 = serious reassessment needed. The list is diagnostic, not predictive; partnership decisions still depend on firm-specific dynamics.

PQE 1-3: technical depth checklist

- [ ] You’ve narrowed to one practice area and can defend that choice

- [ ] You’ve drafted at least 3 transaction documents end-to-end (not just sections)

- [ ] You can run a basic regulatory-tracker check without senior input

- [ ] At least one senior associate or partner trusts you with weekend turnaround work

- [ ] You’ve attended at least 2 client meetings (silent or observing counts)

- [ ] You read the firm’s client alerts and at least 2 industry publications weekly

- [ ] You can name 5 in-house counsels at clients you’ve supported

- [ ] You’ve had at least 1 formal mid-year review with documented feedback

- [ ] Your A1-to-A2 or A2-to-A3 promotion was on the standard cycle, not delayed

- [ ] You’ve turned down at least 1 non-strategic ask to protect priority work

PQE 4-6: BD and visibility checklist

- [ ] You’ve co-authored or solo-authored at least 2 client alerts under your byline

- [ ] You’ve spoken at one industry forum (panel, breakfast, or webinar)

- [ ] You can name a senior partner who would publicly back your case in committee

- [ ] You’ve referred at least 2 client matters to other practices within the firm

- [ ] You’ve met 10+ in-house counsels at target clients and exchanged business cards

- [ ] You’ve been the primary firm-side relationship lead on at least 1 mid-size matter

- [ ] You’ve trained at least 2 A1-A3 associates and built reciprocal trust with them

- [ ] Your billable hours are within 10% of the firm’s PA expectation (typically 2,200+)

- [ ] You’ve contributed at least 1 firm-internal initiative (DEI, KM, training)

- [ ] Your last review explicitly mentioned partnership-track signals (or you’ve asked why not)

PQE 7-9: partnership-vote-readiness checklist

- [ ] You’ve originated at least 1 standalone client retainer

- [ ] You’ve documented INR 2-5 crore in originated or sustained client billings

- [ ] At least 2 senior partners have publicly mentioned you as partner-eligible in the last 12 months

- [ ] You can pay or finance the firm’s expected capital buy-in within 6 months

- [ ] You’ve led at least 1 firm-wide initiative (practice-build, lateral hiring, M&A integration)

- [ ] You have a documented practice-build plan for years 1-3 as partner

- [ ] You’ve successfully managed at least 1 difficult client situation end-to-end

- [ ] You’re actively cross-selling to at least 3 other practice heads

- [ ] You’ve built relationships with the partnership committee or managing partner directly

- [ ] You’ve turned down at least 1 lateral offer in the last 12 months on track-conviction grounds

Red flags: 7 signals you may be being managed out

- You’ve been removed from priority deal teams without a clear practice-area shift explanation

- You haven’t had client-facing time in over 6 months despite asking for it

- You’ve been offered Counsel without a written conversion plan to partner

- Your last 2 reviews avoided partnership-track language entirely

- You’re being asked to mentor laterally rather than upward (admin signal)

- Your originated billings have flatlined for 18+ months while peers’ have grown

- A senior partner who used to involve you in pitches has stopped without explanation

The pitfall: treating the checklist as deterministic. It’s diagnostic. A 9/10 score still depends on firm-specific dynamics and the leverage math; a 6/10 score is fixable in 12-18 months if you focus on the right items.

PQE 1-3 – Technical Depth

- You’ve narrowed to one practice area and can defend that choice

- You’ve drafted at least 3 transaction documents end-to-end (not just sections)

- You can run a basic regulatory-tracker check without senior input

- At least one senior associate or partner trusts you with weekend turnaround work

- You’ve attended at least 2 client meetings (silent or observing counts)

- You read the firm’s client alerts and at least 2 industry publications weekly

- You can name 5 in-house counsels at clients you’ve supported

- You’ve had at least 1 formal mid-year review with documented feedback

- Your A1-to-A2 or A2-to-A3 promotion was on the standard cycle, not delayed

- You’ve turned down at least 1 non-strategic ask to protect priority work

PQE 4-6 – BD and Visibility

- You’ve co-authored or solo-authored at least 2 client alerts under your byline

- You’ve spoken at one industry forum (panel, breakfast, or webinar)

- You can name a senior partner who would publicly back your case in committee

- You’ve referred at least 2 client matters to other practices within the firm

- You’ve met 10+ in-house counsels at target clients and exchanged business cards

- You’ve been the primary firm-side relationship lead on at least 1 mid-size matter

- You’ve trained at least 2 A1-A3 associates and built reciprocal trust with them

- Your billable hours are within 10% of the firm’s PA expectation (typically 2,200+)

- You’ve contributed at least 1 firm-internal initiative (DEI, KM, training)

- Your last review explicitly mentioned partnership-track signals (or you’ve asked why not)

PQE 7-9 – Partnership-Vote Readiness

- You’ve originated at least 1 standalone client retainer

- You’ve documented INR 2-5 crore in originated or sustained client billings

- At least 2 senior partners have publicly mentioned you as partner-eligible in the last 12 months

- You can pay or finance the firm’s expected capital buy-in within 6 months

- You’ve led at least 1 firm-wide initiative (practice-build, lateral hiring, M&A integration)

- You have a documented practice-build plan for years 1-3 as partner

- You’ve successfully managed at least 1 difficult client situation end-to-end

- You’re actively cross-selling to at least 3 other practice heads

- You’ve built relationships with the partnership committee or managing partner directly

- You’ve turned down at least 1 lateral offer in the last 12 months on track-conviction grounds

Red Flags

If 2 or more apply, your track is at risk – escalate or plan a move.

- You’ve been removed from priority deal teams without a clear practice-area shift explanation

- You haven’t had client-facing time in over 6 months despite asking for it

- You’ve been offered Counsel without a written conversion plan to partner

- Your last 2 reviews avoided partnership-track language entirely

- You’re being asked to mentor laterally rather than upward (admin signal)

- Your originated billings have flatlined for 18+ months while peers’ have grown

- A senior partner who used to involve you in pitches has stopped without explanation

After partnership: what actually changes (and what doesn’t)

Most associates plan their lives until the partnership announcement. Almost none plan what happens after. Here’s the post-partner reality.

The first-year-as-partner reality

The first year as a fresh equity partner involves four parallel adjustments. Capital call: most firms require the buy-in within 90 days. BD pressure: from day one, you’re expected to bring in originated work, even if you’re still managing legacy client relationships. Team management: you now own a team’s P&L, not just your own time. Less drafting: junior partners delegate first-draft work downward; you’re reviewing and signing off, not writing.

Can a partner be fired in India?

Yes. Firms can ask a partner to leave through several mechanisms: capital return on equity unit, expulsion vote (rare but exists at vote-driven firms), or quiet performance management leading to a negotiated exit. The most common pattern is the negotiated exit: firms don’t usually expel, but they make staying uncomfortable for partners whose books or behaviour fall below firm standards. Track length to expulsion or exit is typically 18-30 months from the first formal performance flag.

From NEP to EP: the second promotion most associates don’t anticipate

For most associates, NEP feels like the destination because the title says “Partner.” It isn’t. At most Tier-1 Indian firms, NEP is a 2-4 year gate before EP. Some NEPs convert; others don’t. The conversion factors are familiar from earlier sections: originated revenue, capital readiness, and continued sponsorship. The pitfall: assuming NEP equals EP when it doesn’t. Plan for the second gate, not just the first.

Frequently asked questions about the law firm partnership track in India

How many years does it take to become a partner at a top Indian law firm?

The law firm partnership track in India typically runs eight to ten years to non-equity partner, and nine to thirteen years to equity partner at Tier-1 firms. Corporate practice runs the fastest; litigation runs the longest. The 2014 Legally India study found a 9.1-year average across CAM, AZB, JSA, Khaitan, Luthra, and Trilegal, and 2025 forum data confirms the same band. Big 4 legal arms run 15-16 years.

What is the difference between a salaried partner and an equity partner in India?

Salaried partners draw fixed pay plus bonus, don’t share in firm profits, and typically don’t vote on partnership matters. Equity partners contribute capital, share in firm profits, vote on key decisions, and bear downside risk. Salaried partner can be a waypoint or a permanent designation, depending on the firm. At several Indian firms, NEP sits between salaried and equity.

How much does a partner earn at CAM, AZB, Khaitan, Trilegal, SAM, and JSA?

Non-equity partners at Tier-1 firms typically earn INR 80 lakh to 1.2 crore. Fresh equity partners earn INR 1.5 to 4 crore. Senior equity partners and practice heads earn INR 4 to 10 crore-plus. Vahura’s 2024-25 data shows large-firm 10+ PQE median compensation at INR 104.9 lakh. Numbers vary by practice area, origination, and firm tier.

What is the typical hierarchy in an Indian law firm?

The standard ladder runs A0, A1, A2, A3, Senior Associate, Principal Associate, Counsel, Salaried Partner, Non-Equity Partner, Equity Partner, then Senior Equity / Practice Head / Managing Partner. Several firms also use parallel tracks like Counsel, Of-Counsel, Director, Associate Partner, and Responsible Partner. Rung names mean different things at different firms.

Can a non-advocate be a partner in an Indian law firm?

Under the Indian Partnership Act, 1932, partners need not be advocates. But Bar Council and law-firm conduct rules mean almost all partners at traditional law firms are enrolled advocates. Non-advocate partnerships are common at consulting-style legal services entities. At a traditional firm, expect Bar Council enrolment as a practical prerequisite even where the statute doesn’t formally require it.

What is a “book of business” and when should an associate start building one?

A book of business is the client revenue you originate and retain for the firm. At Indian Tier-1 firms, equity-partner-track associates should start visible BD activity by PQE 4-5, earlier than the conventional “after senior associate” advice. By PQE 7, BD is expected, not optional. Origination credit, retained-client billings, and cross-practice referrals all count toward the book.

Is there a capital buy-in for equity partnership in Indian firms?

Yes at most equity-partnership firms. Buy-in ranges from INR 25 lakh at smaller firms to over INR 1 crore at top-tier firms, depending on the equity unit acquired. It’s usually paid from accumulated bonuses or financed through firm-arranged loans repaid against profit share over three to five years. If you can’t pay, firms typically route candidates to NEP or Counsel instead.

What is “Counsel” or “Of Counsel” in an Indian law firm?

Counsel is a formal mid-to-senior tier between Principal Associate and Partner, used by Khaitan, Trilegal, ELP, IndusLaw, and SAM. At Trilegal it’s a real partnership-track waypoint, with the April 2025 round elevating eight Counsels to Equity Partner. Of-Counsel is typically a senior practitioner attached to the firm without partnership economics, voting rights, or capital contribution.

What is a “Principal Associate”?

The senior-most associate rung before Counsel or Salaried Partner, typically PQE 5-7. It can be a real promotion stop or a parking slot, depending on the firm and practice area. The cleanest test is to ask the conversion-rate-to-Counsel-or-Partner of past PA cohorts at the firm. If the firm dodges the question, treat it as a parking slot.

How many billable hours does an Indian Tier-1 associate work per year?

Two thousand two hundred to three thousand logged billable hours per year is the typical Tier-1 range. Total worked hours often exceed three thousand five hundred. That maps to 60-70 hour weeks for most of the year, with peaks above 80 in transaction crunch. Litigation associates’ chargeable patterns differ; court time and case-research time fold in differently from corporate billable structures.

Why do most associates never make partner?

Three structural reasons. First, the leverage ratio: at 1:6 partner-to-associate, math limits promotions to roughly 16% of any cohort. Second, book-building is the gating skill, and few associates start early enough. Third, lateral churn at PQE 4-7 thins the cohort before partnership decisions are made. Merit alone is not enough; sponsorship and originated revenue do most of the work.

Can I make partner without a senior partner sponsor?

Possible but rare. Sponsorship, where a senior partner publicly backs your case in committee, is how most equity nominations actually get through. Without one, the path requires a portable book of business so strong that the firm cannot afford to lose you to a competitor. That’s a small, hard-to-reach minority. Build sponsorship deliberately from PQE 5 onwards.

How do BCI rules on foreign law firms (2023 + May 2025) affect the partnership track?

The March 2023 BCI rules permit foreign lawyers and firms to register on a reciprocity basis, restricted to foreign and international law (not Indian law, not court appearance). The May 2025 IFLF clarification allows Indian-foreign law firm collaborations on non-litigious foreign work. Effect: a new India-office partner tier paying in USD or EUR is emerging, pulling Tier-1 senior associate and counsel talent.

Will AI shrink the path to partnership in Indian firms?

AI compresses the associate funnel. Tools like VIDUR AI reclaim approximately 30% of billable hours and materially compress research and drafting cycles, per BDO and Trilegal commentary. Junior cohorts are shrinking. Partnership criteria are hardening around BD, client management, and judgement, capabilities AI cannot replace. Track length may shorten, but the gate gets narrower for those who specialised purely in technical research.

Is making partner in India still worth it in 2026?

Mixed answer. On the law firm partnership track in India, equity partner economics remain strong: INR 1.5-4 crore fresh, INR 4 crore-plus senior. But salaried partner pay overlaps with senior in-house GC pay (INR 1.5-3 crore plus RSU) for fewer hours. The case for partnership is strongest when you want firm equity, governance influence, and long-tail wealth, not just a higher current salary. Match the path to your goals.

What is the gender ratio of partners at top Indian law firms?

Approximately 30% women across India’s top 30 firms, per Legally India and Bar and Bench data. Roughly 15% in litigation seniority. Outliers exist; Samvad Partners reports approximately 64% women partnership. The ratio is close to parity at junior associate levels and compresses sharply at Counsel-and-above. Structural reasons (partnership timing colliding with childcare years, sponsor scarcity) are well-documented.

Litigation vs corporate, which has the faster partnership track?

Corporate is meaningfully faster. Four of Trilegal’s April 2025 EP cohort were corporate; CAM and Khaitan corporate-heavy promotion rounds confirm the pattern. Litigation runs a leaner pyramid: fewer slots, longer tracks (often 11-14 to EP), but lower leverage means partner-share economics can be stronger per partner. Match practice area to your timing tolerance and lifestyle preference.

How does an Indian law firm partner’s pay compare to an in-house General Counsel?

NEP pay (INR 80 lakh to 1.2 crore) overlaps with senior GC pay (INR 1.5-3 crore plus RSU at MNCs); EP pay clears it. But in-house GCs work 900-1,100 hours per year against partners’ 2,500-plus. Per-hour, GC often wins; total-comp peak, EP wins. The decision is about lifestyle, equity ownership, and time horizon, not just cash. Pick what you actually want.

This article is for informational purposes only and does not constitute legal advice. For specific career or legal guidance, consult a qualified legal professional.